In South African finance, Generative AI is moving from theory to practice by addressing local challenges like social inclusion and regulatory compliance. The technology enhances risk management with richer data, automates complex operational workflows, and breaks down language barriers, requiring a specific strategy that balances innovation with accountability.

For global financial markets, Generative AI presents a frontier of innovation. But for South Africa, it represents something more immediate: a complex tool to be applied to our unique set of economic and social challenges.

The conversation in our boardrooms is shifting from the hypothetical to the practical. We're progressing from generic machine learning capabilities and asking tougher, more specific questions. How can this technology serve our diverse, multilingual population? How do we administer it within our specific regulatory frameworks like 'Twin Peaks' and POPIA? And how do we manage the extreme operational and human shifts it demands?

This is the South African financial renaissance, and it requires a uniquely South African strategy.

The Legacy Foundation: How Predictive Analytics Set the Stage

Traditional machine learning models gave us a strong foundation, particularly in refining credit scoring and identifying known fraud patterns. But these models depended almost exclusively on structured, historical data. Their view of risk was backward-looking.

In the South African context, particularly considering our large informal economy and dynamic population, this approach would penalise gig workers and other informal earners. It strengthened existing biases because it lacked the data to understand their economic lives. The traditional models struggled to keep pace with how quickly fraud behaviour was changing, especially as fraudsters developed more sophisticated tactics.

Generative AI operates on a different level. Its ability to ingest and interpret vast quantities of unstructured and multi-modal data (from WhatsApp messages and voice transcripts to documents) provides a much richer, more current picture of risk. It supports dynamic, real-time reasoning, allowing us to identify and react to novel fraud scenarios, like complex SIM-swap or synthetic identity fraud, without needing explicit prior examples.

This hugely reduces the model-lag risk that left us vulnerable. Instead of just producing a score, GenAI can generate a full risk narrative that combines transactional data with behavioural context and external signals. This gives credit analysts and fraud investigators outputs that are easier to interpret, resulting in faster, more confident decisions.

Key Takeaway: Generative AI improves upon older predictive models by analysing diverse, unstructured data to create a richer, real-time view of financial risk.

Operational Efficiency: Transforming the Middle Office and Compliance

While risk management has seen a significant evolution, the most surprising breakthrough from GenAI in the last year has been in simplifying document-heavy operational workflows. Processes like insurance claims, customer onboarding, and FICA compliance have historically been manually intensive, expensive, and prone to human error.

Machine learning made inroads, but GenAI is fundamentally reshaping these functions. It can read and make sense of messy, unstructured documents (like scanned IDs, handwritten forms, proof of address PDFs) and then extract, standardise, and summarise the critical data within them. This capability is drastically reducing the need for manual document review.

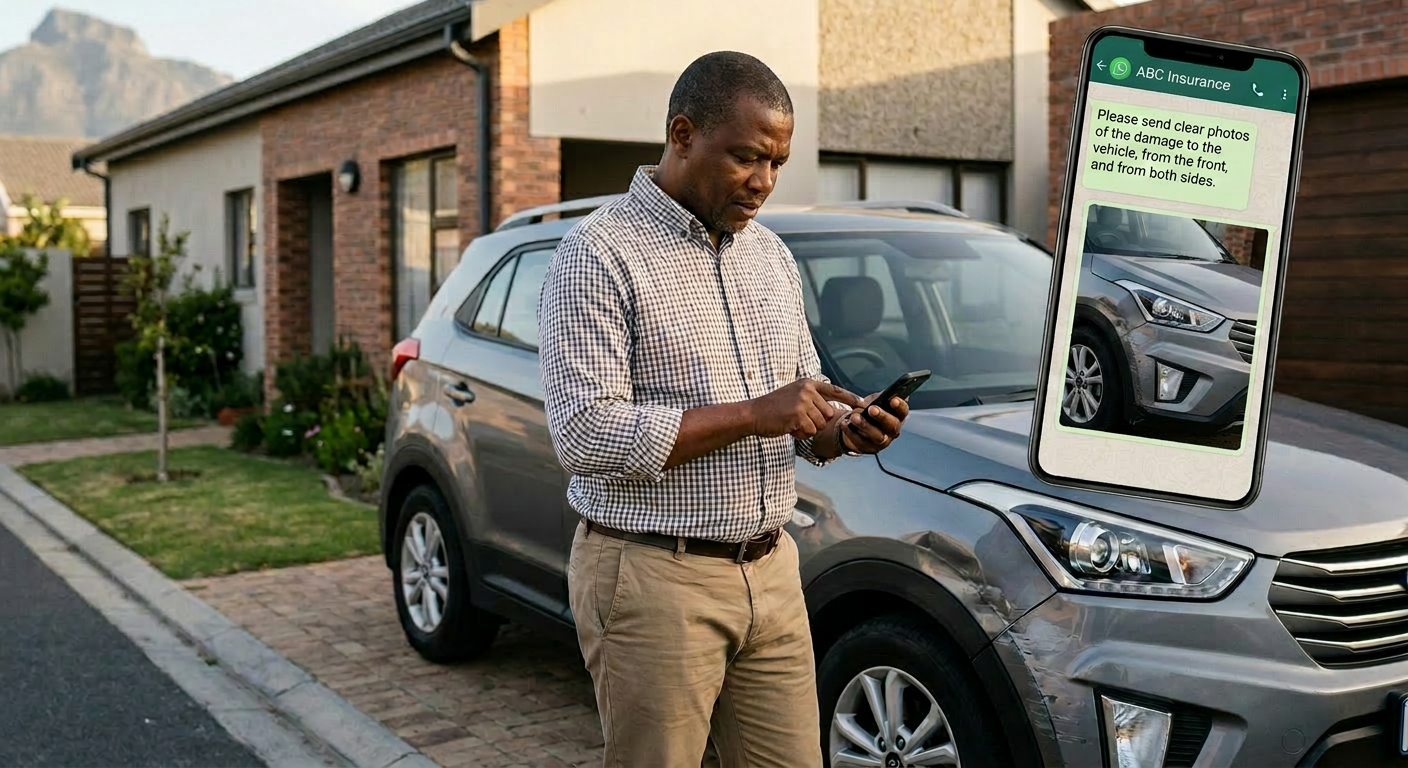

This is especially evident in insurance claims. What used to be a chain of emails and form-filling can now be initiated through a simple WhatsApp bot which can process the initial claim, check for inconsistencies, and move it forward. This means claims are settled faster, with fewer errors, and a reduced back-office burden.

For customer onboarding, the technology reviews identity documents and financials, flagging missing information and generating compliance-ready summaries. The impact is quantifiable. 83% of South African firms report productivity improvements directly attributable to GenAI, while 86% of users cite increased competitiveness and 66% see enhanced customer service. [1]

Human-agent efficiency is being boosted by AI co-pilots. The retrieval of policy information and drafting responses to customers can now happen in seconds, freeing the agents up to focus on complex customer queries that require human intervention.

Key Takeaway: GenAI is driving major productivity gains by automating document-intensive processes like claims and customer onboarding, reducing manual work and errors.

The Regulatory Pulse: A Pragmatic Path for SARB and FSCA

It is essential that regulation keeps pace with the rapid evolution of these powerful tools. South Africa, though, should be careful not to copy global frameworks without considering the intricacies of our own market.

The EU AI Act, for example, focuses heavily on classifying the models themselves and deciding whether they are “high-risk”, but our regional market demands a more practical approach. We should regulate the use-case, not the model. The same generative AI tool could help a bank draft a simple marketing email in one setting, and support a high-stakes trading decision in another. The technology is not the whole risk. The real risk depends on how, where, and why it is used.

For an institution like the South African Reserve Bank (SARB), attempting to monitor and classify every model is likely infeasible. We don’t have the same state-level technical infrastructure as the EU, and heavy model-level regulation could stifle the very fintechs that are making strides in financial inclusion.

A more sensible approach would be to define a set of critical financial AI use-cases. Credit underwriting, insurance pricing, and fraud detection should sit in the high-scrutiny category. Those areas need proper outcome audits and a clear way for humans to step in when needed.

But not every AI use-case carries the same level of risk. A customer service chatbot, for example, should not face the same regulatory burden as an AI system influencing someone’s access to credit. For lower-risk tools, the focus should be on transparency, disclosure, and clear escalation paths.

Employing a use-case-based approach aligns with the spirit of TFC (Treating Customers Fairly), ensuring we can prove that our decisions are fair and explainable. This is exactly what regulators want to see.

Key Takeaway: South Africa's financial regulators should focus on governing how AI is applied in specific high-risk scenarios, rather than attempting to regulate the AI models themselves.

Personalisation at Scale for a Diverse Nation

For decades our South African financial sector has been limited by language. The English-first approach excluded large segments of our population, giving rise to mistrust. This hampered the adoption of digital banking services. With the advent of GenAI we are finally able to bridge this divide. Local banks are now eclipsing the capabilities of global models by integrating language-native AI that understands our unique dialects, slang, and context. As a result, voice-first interactions are becoming as important as text.

ABSA Bank's ChatWallet on WhatsApp, for instance, serves thousands of customers in English, isiZulu, Sesotho, and Afrikaans. The real challenge wasn’t the core technology. It was mastering the linguistic and cultural nuances, like code-switching, to avoid misinterpretation.

By deploying on a low-data platform like WhatsApp, services such as payments, loan applications, and buying electricity are now accessible to rural and low-income earners who found traditional banking apps too data-intensive.

This is also how we're tackling financial inclusion for the 'unbanked'. Where historical data is thin, GenAI enables alternative credit scoring. By analysing data points like mobile money usage and transaction semantics, we can assess the creditworthiness of informal earners who were previously invisible to the financial system.

Key Takeaway: By supporting multiple local languages and enabling alternative credit scoring, GenAI is making financial services more accessible and inclusive across South Africa.

Strategic Roadblocks: Ownership, Talent, and Technical Debt

Despite the clear potential, many firms find themselves stuck in 'pilot purgatory'. While there's a tendency to blame poor data quality or legacy systems, the single biggest barrier observed is a cultural one: a lack of clear ownership for decisions that are influenced or made by AI.

In a pilot, a human is always there to review and sign off, remaining fully accountable. But in production, an AI might influence pricing, underwriting, or claims triage. These are decisions with real-world consequences. Under regulations like TCF and SAM reporting, accountability is everything. Who is the formal risk owner when an AI gets it wrong? Is it IT, the actuarial team, or compliance? Without a clear answer, boards remain hesitant to scale.

This leads directly to the question of technical strategy. Building proprietary Large Language Models (LLMs) from scratch is financially and technically unrealistic for most South African firms. It requires massive compute power and advanced skills that are still scarce locally.

Instead, the dominant architecture emerging is a hybrid one: using a global base model, layering on internal data via Retrieval-Augmented Generation (RAG), and then applying targeted fine-tuning to inject proprietary business logic and regulatory rules. This approach is faster, more cost-effective, and mitigates compliance risk, especially concerning data sovereignty under POPIA. It’s a pragmatic solution born from our specific constraints.

Key Takeaway: The primary obstacle to scaling GenAI in finance is the cultural challenge of assigning clear ownership and accountability for AI-influenced decisions.

The Future Outlook: A 'GenAI-First' Financial Institution

The long-term workforce implications of this shift are profound. Some executives are blunt, seeing routine call centre and branch roles shrinking dramatically as a result of substitution by AI. And they're not wrong. The cost savings are too significant for shareholders to ignore. We could see AI systems handling 70-90% of routine customer interactions autonomously by 2027. Humans will increasingly be reserved for moments requiring complex judgment, regulatory exceptions, or genuine emotional intelligence.

This will reshape our financial institutions. Instead of a thousand call centre agents, a bank might employ 200 highly skilled 'AI-augmented advisors' who handle escalations. New roles like 'Conversation Designer' and 'AI Interaction Supervisor' will emerge to fine-tune and monitor these systems.

While some firms are piloting 'horizontal redeployment' programmes to move staff into oversight roles, the reality check is that not every entry-level employee can be retrained for a data or compliance position. The skill gap is real. Building a 'GenAI-first' institution in South Africa will require a measured approach, balancing the immense potential for efficiency and inclusion with a clear-eyed strategy for workforce transition.

Key Takeaway: GenAI will replace many routine financial service jobs with fewer, more specialised roles, requiring a strategic focus on workforce transition and reskilling.

Conclusion

The journey from traditional machine learning to generative AI is a fundamental strategic pivot for the South African financial sector. It demands that we look beyond the global hype and focus on practical, regulated implementation that addresses our specific market needs.

The potential is real. GenAI can help banks and insurers break down language barriers, make credit scoring more inclusive, and take some of the friction out of compliance. But the hard questions are just as real. Who owns the risk when AI influences a decision? How do we protect customers? And what happens to the people whose roles will change?

Success will not come from adopting the technology fastest, but from embedding it most thoughtfully within our strategic, regulatory, and social context.

Sources

Key Definitions

Generative AI (GenAI)

A type of artificial intelligence capable of creating new content, such as text and summaries, by learning from vast amounts of data. In finance, it is used to analyse unstructured information like documents and messages to improve risk assessment and automate operational tasks.

Use-Case-Centric Regulation

A regulatory philosophy that applies rules based on how an AI technology is used (its application), rather than on the underlying technology itself. This allows for stricter controls on high-risk activities like credit scoring while permitting more flexibility for low-risk ones.

Pilot Purgatory

A common situation where a company successfully tests a new technology in a small-scale trial (a pilot) but fails to implement it into full, company-wide production due to internal barriers like lack of ownership, regulatory uncertainty, or cultural resistance.

Retrieval-Augmented Generation (RAG)

A technique for making Generative AI more accurate and context-aware. It involves combining a large, pre-trained language model with a company's own secure, internal data, allowing the AI to 'retrieve' specific information before generating a response.

Alternative Credit Scoring

A method of assessing a person's creditworthiness using non-traditional data sources, such as mobile money usage or transaction patterns. This is particularly useful for individuals in the informal economy who lack a formal credit history.

Frequently Asked Questions

How does Generative AI differ from older machine learning models in finance?

Generative AI can interpret vast amounts of unstructured data, like WhatsApp messages and documents, to provide a current picture of risk. Unlike older models that relied on historical, structured data, GenAI can identify new fraud patterns in real-time and produce full narrative explanations for its decisions, rather than just a score.

What is the biggest operational benefit of GenAI in South African banking and insurance?

The most significant benefit has been the simplification of document-heavy workflows. GenAI automates processes like insurance claims, customer onboarding, and FICA compliance by reading unstructured documents, extracting key data, and summarising it, which reduces manual errors and operational costs.

How should South Africa approach the regulation of Generative AI in finance?

A pragmatic approach for South Africa is to regulate the specific 'use-case' of the AI, not the AI model itself. This means high-scrutiny applications like credit underwriting would have mandatory audits and human oversight, while lower-risk uses like marketing would face a lighter touch, fostering innovation while ensuring fairness.

How does GenAI promote financial inclusion in South Africa?

GenAI helps bridge the language divide by powering services in multiple local languages and dialects, making digital banking accessible to more people on low-data platforms like WhatsApp. It also enables alternative credit scoring by analysing data like mobile money usage, allowing financial institutions to assess the creditworthiness of informal earners previously excluded from the system.

What is the main barrier preventing insurers from scaling GenAI projects?

The single biggest barrier is not technical, but cultural. It is the lack of clear ownership and accountability for decisions influenced or made by AI. With regulations demanding clear accountability, firms are hesitant to move beyond pilots until there is a formal risk owner for AI-assisted decisions in areas like pricing and underwriting.

What is the expected impact of GenAI on financial sector jobs in South Africa?

GenAI is expected to handle 70-90% of routine interactions by 2027, leading to a significant reduction in roles like call centre agents. The workforce will shift towards fewer, but more highly skilled, 'AI-augmented advisors' who manage complex escalations and exceptions, requiring a deliberate strategy for workforce transition.

Keywords: Generative AI, Financial Services, South Africa, Fintech, Regulation, Digital Transformation, Financial Inclusion, Risk Management