TL;DR

Generative AI is revolutionising South Africa's financial sector by streamlining document-heavy processes, enhancing financial inclusion through multilingual support, and enabling advanced fraud detection. This transformation goes beyond traditional Machine Learning, addressing critical operational bottlenecks and fostering a "GenAI-First" approach while navigating a complex regulatory environment.

Why Generative AI is Reshaping South Africa's Financial Sector

The South African financial sector is rapidly moving beyond traditional Machine Learning (ML) to adopt Generative AI (GenAI). While ML brought foundational improvements to areas like credit scoring and fraud detection, GenAI is now uncovering novel efficiencies and opportunities that specifically cater to South Africa's distinct economic and social landscape. This isn't just a minor tech update, it's a substantial re-architecture of how financial institutions function, serve customers, and manage risk.

This strategic shift redefines operational bottlenecks, boosts financial inclusion, and adds a new dimension to risk assessment, aligning global technological advances with local needs in a dynamic market.

Key Takeaway: GenAI is fundamentally reshaping the South African financial sector, moving beyond ML to address unique local needs and operational bottlenecks.

How Predictive Analytics Paved the Way for GenAI

Traditional Machine Learning models formed the analytical foundation for South African finance for years. These models excel at processing structured data, bringing precision to tasks like credit risk assessment and fraud detection. They allowed banks and insurers to make better-informed decisions, replacing basic rule-based systems with sophisticated predictive analytics. For instance, ML algorithms refined credit scoring by analysing vast datasets of repayment histories, income stability, and demographic information.

However, these models depend on well-organised, quantifiable data. Their training is typically periodic, requiring regular updates to adapt to evolving patterns, especially in the fluid landscape of financial fraud. In South Africa, with its large informal economy and diverse transactional behaviours, this reliance on structured data often meant that segments of the population, such as gig workers or those outside formal employment, were underserved or excluded. Despite their sophistication, these foundational ML systems highlighted the limitations of a purely structured data approach, setting the stage for GenAI innovation.

Key Takeaway: Traditional ML models, while precise with structured data, revealed limitations in diverse South African contexts, creating a need for GenAI.

Where Generative AI Transforms Operations

While traditional ML established the groundwork, Generative AI is now creating entirely new efficiencies, particularly in streamlining document-heavy processes that were historically prone to inefficiency and error within South African financial institutions. Claims processing and customer onboarding serve as prime examples.

These workflows traditionally required significant manual intervention, leading to delays, inconsistencies, and high operational costs. Now, GenAI interprets messy, unstructured documents, extracts and standardises critical data, summarises context, and even automates responses or decisions. This capability dramatically reduces the manual review needed in onboarding, compliance checks, and claims handling.

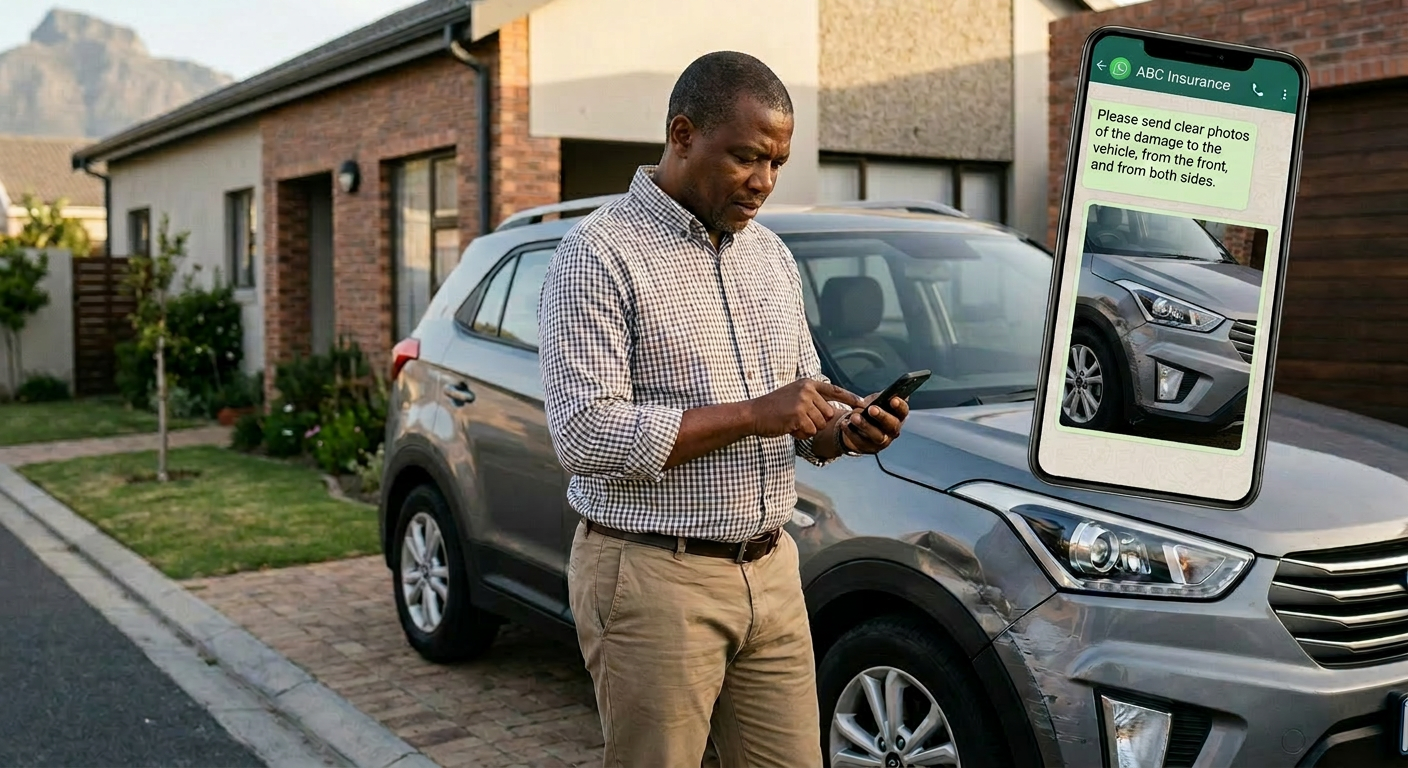

For instance, in insurance claims, GenAI has revolutionised the process, shifting from tedious form-filling and emailing to submissions via chat or WhatsApp bots. This results in faster claim settlements, fewer errors, and a lighter back-office load. For Know-Your-Customer (KYC) onboarding, GenAI eliminates manual review of IDs, proof of address, and financial statements; it flags missing data or inconsistencies and generates compliance-ready summaries, ensuring faster, more accurate regulatory adherence.

AI co-pilots further support agents by instantly retrieving policy information, summarising customer context, and drafting responses, freeing them from time-consuming searches across various systems. The impact is clear. According to findings from the South African Generative AI Roadmap 2025, reported by ITWeb, 83% of South African GenAI users reported improved productivity, while 86% cited increased competitiveness and 66% reported enhanced customer service. [1]

Key Takeaway: GenAI drastically improves operational efficiency by automating document-heavy processes like claims and onboarding, leading to significant productivity gains.

How Regulators are Approaching GenAI

South Africa's financial regulators, including the South African Reserve Bank (SARB) and the Financial Sector Conduct Authority (FSCA), are closely monitoring AI deployment. They acknowledge its immense potential but also its inherent risks, particularly regarding accountability and fairness. Rather than regulating GenAI based on what it is, a model, South African regulators may need to focus on what it is used for; recognising that the same technology can carry very different levels of risk depending on its application. The same GenAI model can generate harmless marketing copy one moment and, if misapplied to automated trading, trigger systemic risk the next; the context amplifies its impact.

Regulating models at the technological layer, as seen in some European and American frameworks, might be impractical for South Africa. South Africa does not have the same level of technical infrastructure as the EU, and overly burdensome regulation could constrain smaller fintechs that play an important role in advancing financial inclusion for underserved communities. Instead, SARB could define 'critical financial AI use-cases': high-scrutiny domains like insurance pricing, credit underwriting, and fraud detection. These applications would require mandatory outcome audits and human override capabilities.

Conversely, low or moderate scrutiny domains, such as marketing content generation or customer service chatbots, could have minimal regulatory burden, focusing more on disclosure and transparency. This approach aligns with the FSCA's mandate for plain language explanations and 'Treating Customers Fairly' (TCF) even when AI is involved, ensuring decisions are auditable and understandable, and addressing concerns about 'black box' biases.

Key Takeaway: South African regulation should focus on financial AI use-cases rather than the models themselves, balancing innovation with accountability.

GenAI in Retail Banking: Personalised and Inclusive for a Diverse Population

For South African retail banking, Generative AI presents an unprecedented opportunity to address the country's unique demographic needs and digital divide. Traditional English-only banking applications have historically excluded large segments of the population, leading to misunderstandings of financial products, reduced trust, and lower adoption of digital services. GenAI is changing this dynamic by enabling truly language-native and context-aware interactions. Integrated language-native AI is emerging that goes beyond simple translation, with the ability to understand South African dialects and support voice-first interactions. This is a significant step beyond global models.

Tools like Botlhale enable banks to deploy chatbots in multiple local languages, and platforms now exist that transcribe and analyse multilingual call-centre conversations in real time. This extends beyond merely catering to 11 official languages; it’s about cultural relevance. ABSA Bank's ChatWallet on WhatsApp is a prime example. Launched between 2024-2025, it is positioned to expand access in English, isiZulu, Sesotho, and Afrikaans, offering payments, fund reception, airtime/data/electricity purchases, and loan applications; all through conversational AI.

The greatest challenge wasn't the technology, but fine-tuning for South African slang, which often blends languages, and ensuring alignment with FSCA and POPIA requirements to build trust. By leveraging low-data-usage platforms like WhatsApp, banks are making financial services accessible to rural and low-income earners, effectively using GenAI to bridge the financial inclusion gap exacerbated by traditional systems that penalised informal earners. This move signifies a genuine commitment to serving the entire spectrum of our diverse population.

Key Takeaway: GenAI provides personalised, multilingual financial services in South Africa, bridging the digital divide and promoting inclusion through tools like ABSA's ChatWallet.

Fraud Detection and the POPIA Question

Fraud detection is a practical example of where GenAI can move beyond traditional Machine Learning. While conventional models are strong at identifying known patterns in structured transaction data, GenAI can help interpret unstructured information such as claims descriptions, call-centre notes, WhatsApp messages, supporting documents and customer emails. This allows financial institutions to build a richer risk narrative, identifying inconsistencies, missing evidence and emerging fraud patterns that may not be visible in structured datasets alone.

For South African banks and insurers, the opportunity is significant, particularly in a market where customer behaviour may include informal income, irregular transaction patterns and multilingual communication. GenAI can help distinguish between genuine customer complexity and suspicious behaviour, reducing unnecessary false positives while improving the quality of fraud investigations.

However, this capability also brings POPIA directly into focus. Fraud detection depends on sensitive personal and financial information, and financial institutions must be clear about why the data is being processed, how it is secured, whether it is used to train or fine-tune AI models, and whether any third-party or cross-border processing is involved. POPIA should therefore not be treated only as a regulatory barrier, but as a governance framework for responsible AI design.

The aim should be fraud detection that is faster, but also explainable, auditable and defensible. A GenAI-assisted fraud process should be able to show what data informed the decision, why a case was escalated, when human review occurred and how customer rights were protected.

Key Takeaway: GenAI can strengthen fraud detection by interpreting unstructured customer and claims data, but its use must be governed through POPIA-aligned processes that make every decision explainable, auditable and defensible.

Understanding GenAI Implementation Barriers

Despite GenAI's clear advantages, full-scale adoption in South African financial institutions faces significant strategic roadblocks. Although poor data quality, legacy systems and skills shortages remain important constraints, a more material barrier may lie in the lack of clearly defined accountability among leaders for decisions influenced by GenAI. In pilot phases, GenAI drafts emails or summaries, and a human remains fully accountable. However, with production-level GenAI influencing pricing, underwriting, or claims triage, the implications of an erroneous model can be severe.

South African insurers, operating under SAM reporting and adhering to TCF and FSCA regulations, are inherently risk-averse. These frameworks demand clear accountability, explainable decisions, and defensible outcomes to protect policyholders. Insurers currently lack formal risk ownership structures for AI-assisted decisions. Who owns the risk when an AI makes a critical call? Is it Actuarial, Risk & Compliance, or IT? This ambiguity stalls progress, leading to 'Pilot Purgatory' where innovative projects fail to scale.

Furthermore, the local sector's preference for fine-tuning existing global models over building proprietary LLMs stems not just from cost and capability constraints, but also from regulatory complexities like POPIA and Twin Peaks, which impact data sovereignty and security. Add to this the scarcity of advanced AI skills and limited local compute infrastructure, and you have a landscape ripe with challenges that demand decisive leadership and clear governance to overcome.

Key Takeaway: A lack of clear ownership for AI-assisted decisions, aggravated by regulatory complexities and skills shortages, is the biggest barrier to GenAI scaling.

The Future of Human-in-the-Loop in South African Financial Services

Looking ahead to 2027, the 'Human-in-the-Loop' dynamic in South African financial services will look dramatically different. Routine interactions in financial services are expected to become increasingly AI-assisted or AI-led, while human intervention will become reserved for complex situations where confidence scores dip, regulatory thresholds are triggered, or emotional intelligence is paramount; an area where AI still struggles.

This shift isn't about replacing humans wholesale but re-shaping their roles entirely. New positions are likely to emerge, such as “Prompt/Conversation Designers” who refine AI responses for local context and “AI Interaction Supervisors” who monitor automated conversations and manage escalations.

Branch offices will transform into hybrid spaces, with self-service kiosks and remote advisors becoming more common, and front-line staff supported by AI co-pilots. The regulatory environment will play a critical role in shaping this evolution, likely mandating human override capabilities for AI decisions and requiring robust audit trails to show when AI acted and when humans intervened. While cost pressures and global trends will accelerate AI adoption, skills shortages and digital infrastructure gaps will remain significant constraints.

The candid boardroom conversation acknowledges that while some entry-level roles will inevitably shrink, firms are also exploring 'horizontal redeployment'; reskilling staff into AI supervision, compliance monitoring, or customer coaching. This aims to turn displaced workers into 'AI-augmented advisors' who handle complex cases and regulatory exceptions, aligning with TCF regulations that demand a human escalation path. This measured approach acknowledges the very real human impact of this technological revolution, aiming for a 'GenAI-First' approach that is both efficient and ethically sound for South Africa.

Key Takeaway: By 2027, human roles in finance will shift to AI-augmented advisors handling complex cases, while AI manages routine tasks with mandated human oversight.

Conclusion

Moving from traditional Machine Learning to Generative AI in South Africa's financial sector is more than a technological upgrade; it's a strategic rethinking of operations, customer engagement, and regulatory compliance. The sector is moving beyond the constraints of structured data, increasingly drawing value from unstructured and multi-modal information.

This drives unprecedented efficiencies in areas like claims processing and onboarding, and it fosters deeper financial inclusion through language-native solutions. The regulatory landscape, while carefully monitoring AI's evolution, also has an opportunity to innovate; focusing regulation on the use-case rather than the technology itself.

While challenges remain, particularly around internal ownership of AI-assisted decisions, data privacy, and talent scarcity, the path forward involves a pragmatic blend of global models and local customisation. The future envisions a 'GenAI-First' financial institution where AI handles routine interactions, freeing humans for complex, empathetic tasks, and where new, specialised roles emerge.

This measured yet assertive approach promises to deliver not just efficiency, but also a more inclusive and resilient financial ecosystem for all South Africans.

Sources

Key Definitions

Generative AI (GenAI)

A type of artificial intelligence that can create new content, such as text, images, or decisions, by learning from existing data. It excels at processing unstructured information and automating complex tasks, unlike traditional ML that primarily analyses existing data.

Machine Learning (ML)

A subset of AI that enables systems to learn from data to identify patterns and make predictions or decisions with minimal human intervention. It primarily works with structured data and is used for tasks like credit scoring and fraud detection.

Financial Sector Conduct Authority (FSCA)

The South African market conduct regulator for financial institutions, responsible for ensuring fair treatment of customers, promoting financial stability, and maintaining market integrity.

South African Reserve Bank (SARB)

The central bank of South Africa, responsible for monetary policy, financial stability, and regulating the banking system.

Human-in-the-Loop (HITL)

An AI paradigm where human intervention is explicitly designed into the system to review, adjust, or override AI decisions, particularly when confidence scores are low, or regulatory thresholds are met, ensuring accountability and ethical oversight.

Frequently Asked Questions

How is Generative AI improving efficiency in South African financial institutions?

GenAI simplifies document-heavy processes like claims processing and customer onboarding. It reads unstructured documents, extracts and standardises data, summarises context, and generates decisions, drastically reducing manual review and errors.

How does GenAI address financial inclusion in South Africa?

South African financial institutions use GenAI for multi-language support across all 11 official languages, including voice-first interactions and local dialects. This expands digital banking access, fostering inclusion for populations previously excluded by English-only services.

What is the biggest cultural barrier for South African insurers scaling GenAI projects?

The primary barrier is the lack of clear ownership among leaders for decisions partially made by AI. Current regulations demand clear accountability, creating a governance vacuum for AI-assisted outcomes like pricing and underwriting.

How is GenAI enhancing fraud detection in South African banking?

GenAI interprets unstructured data (e.g., WhatsApp, voice transcripts) to provide a clearer risk picture, especially for informal economy participants. It supports dynamic reasoning for novel fraud scenarios and generates comprehensive risk narratives.

How are banks proving AI-driven credit decisions using alternative data are fair to regulators?

Banks provide plain language explanations for AI decisions, integrate SHAP and LIME for variable influence, conduct bias detection audits across demographic groups, and perform scenario testing to prove fairness, meeting FSCA and POPIA requirements.

By 2027, how will the 'Human-in-the-loop' dynamic evolve in South African financial services?

By 2027, AI systems may handle 70-90% of routine interactions autonomously. By 2027, routine interactions in financial services are expected to become increasingly AI-assisted or AI-led. Human intervention will focus on complex cases with low confidence scores, regulatory triggers, or where emotional intelligence is critical, with new roles emerging for AI supervision and fine-tuning.

Is South Africa's financial sector building proprietary LLMs or fine-tuning global models?

The sector largely focuses on fine-tuning and orchestrating global models (RAG and hybrid architectures). This approach is driven by cost and capability constraints, the need for speed, and regulatory complexities like POPIA and Twin Peaks, rather than building LLMs from scratch.

Keywords

-

Generative AI

-

Financial Sector

-

South Africa

-

Machine Learning

-

AI Regulation

-

Financial Inclusion

-

Operational Efficiency

-

Banking

-

Insurance

-

Karabo More